Sample review engagement financial statements Innisfree

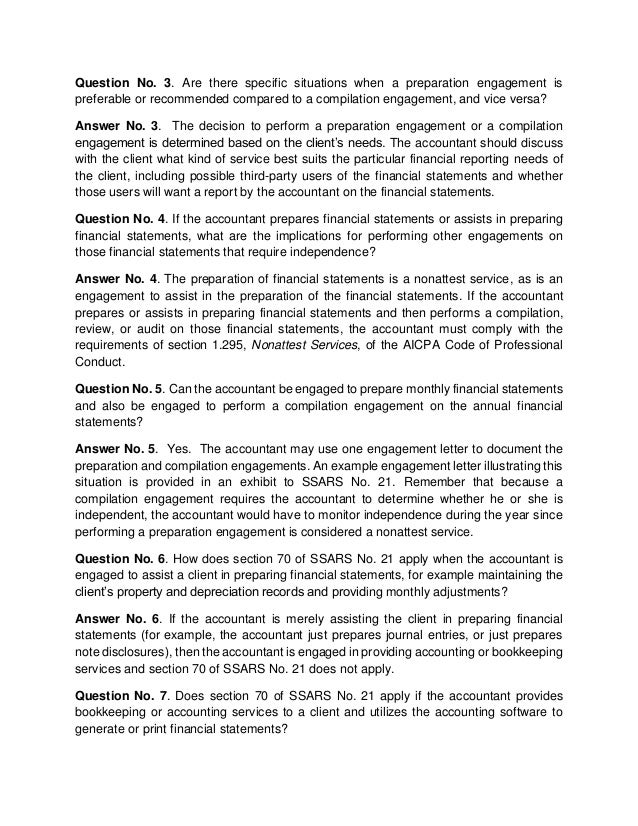

AR-C 70 Preparation of Financial Statements Engagement Are you aware of the option in the SSARS titled Preparation of Financial Statements (AR-C 70)? Many CPAs still believe the lowest level of service in the SSARS is a compilation, but this is not true. CPAs can and do issue financial statements without a compilation report. Today I provide an in-depth look at AR-70, Preparation of Financial Statements. Preparation of Financial Statements

SSARS 21 SSARS 22 SSARS 23 and SSARS 24 update

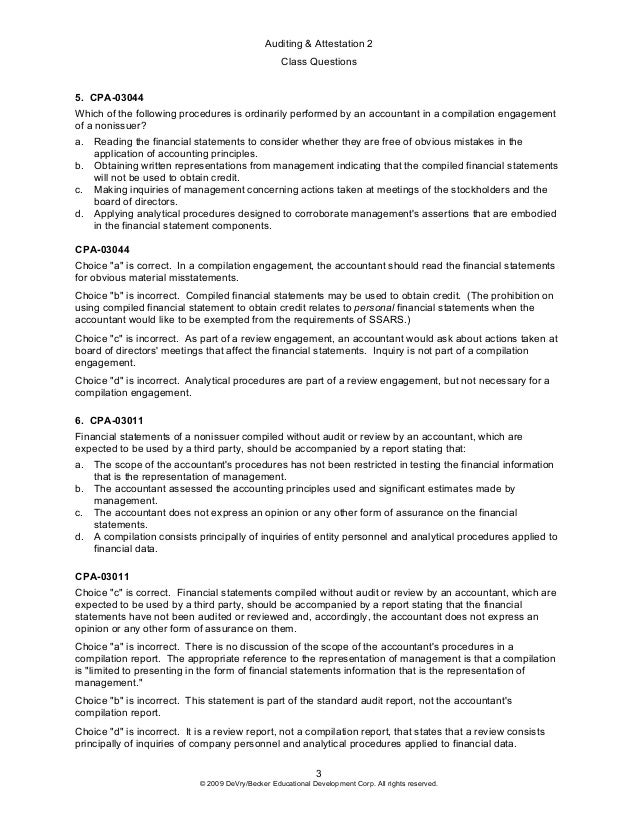

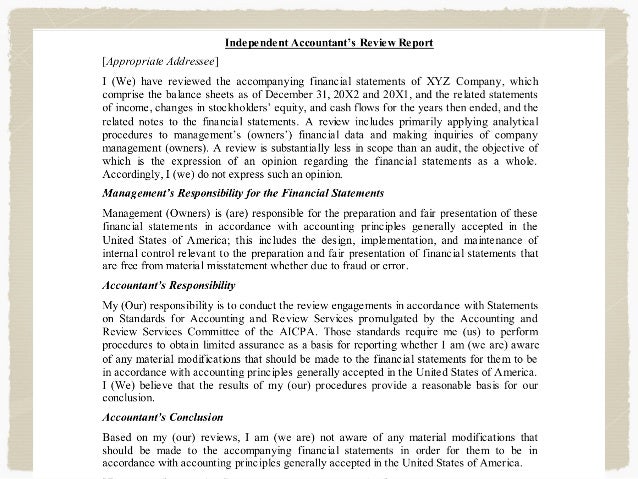

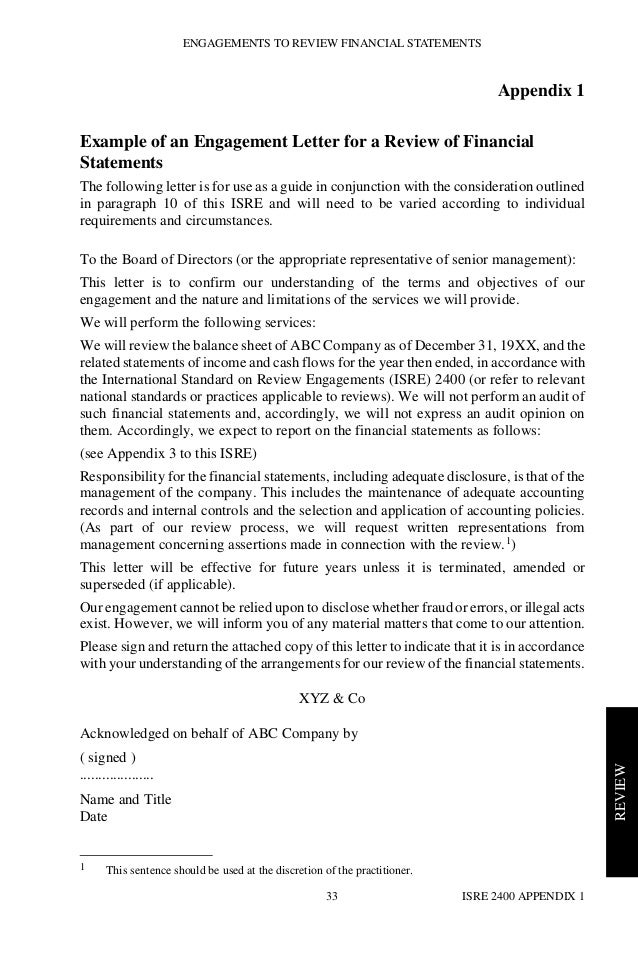

SAMPLE REVIEW ENGAGEMENT LETTER Markel Corporation. For example, hours may be billed weekly or monthly, or a flat fee may be given when the service is complete. If a late payment clause is added, it may be in a separate paragraph. Below is a sample compilation accounting engagement letter. It is intended to be used for the basic CPA services for financial statements. These services may include, Sample Review Report Independent Accountant’s Review Report and the related notes to the financial statements. A review includes primarily applying analytical procedures to management’s financial data and making inquiries of management. A review is substantially less in scope than an audit, the objective of which is the expression of an opinion regarding the financial statements as a.

Example: The best example of review engagement would be the engagement between external audit form to review the client’s financial statements. In normal cases, this kind of engagement, the audit will perform fewer procedures that audit and the assurance that they provided to those financial statements … The general public, and more often, the users of financial statements, appear to lack a basic understanding of the main differences between an audit and a review engagement. ISA 200 explains the purpose of an audit as to enhance the degree of confidence of intended users in the financial statements. This is achieved by the expression of an

Section 70: Preparation of financial statements-- Section 70 provides guidance for accountants engaged to prepare financial statements but not engaged to perform an audit, review or compilation on those statements. An engagement letter is still required for preparing financial statements, signed by the accountant and the client's management. Documentation in Review Engagements This is the seventh and final article in the series highlighting the requirements of the new review engagement standard, Canadian Standard on Review Engagements (CSRE) 2400 – Engagements to Review Historical Financial Statements, which becomes effective for reviews of financial statements for periods ending on or after December 14, 2017, with no option for

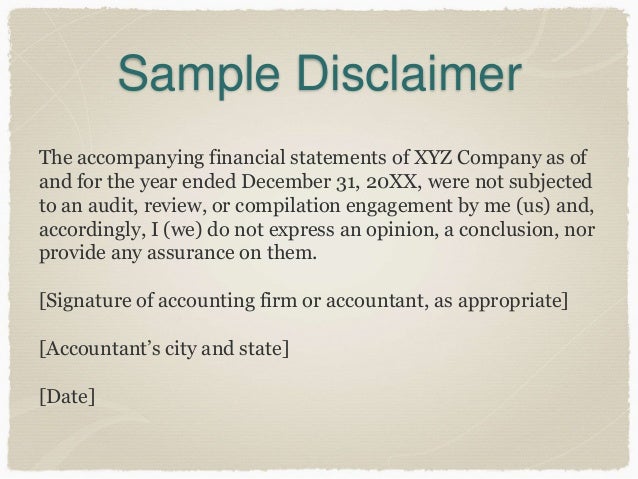

Based on our review, nothing has come to our attention that causes us to believe that these financial statements do not present fairly, in all material respects, the financial position of ABC Company as at February 28, 20X1, and (of) its financial performance and cash flows for the year then ended, in accordance with International Financial Reporting Standards for Small and Medium-sized Entities. be made to the accompanying financial statements in order for them to be in conformity with generally accepted accounting principles. If, for any reason, we are unable to complete our review of your financial statements, we will not issue a report on such statements as a result of this engagement.

Based on our review, nothing has come to our attention that causes us to believe that these financial statements do not present fairly, in all material respects, the financial position of ABC Company as at February 28, 20X1, and (of) its financial performance and cash flows for the year then ended, in accordance with International Financial Reporting Standards for Small and Medium-sized Entities. If, for any reason, I am unable to complete my review of your financial statements, I will not issue a report on such statements as a result of this engagement. It is my policy to keep work papers related to this engagement for seven years. Upon the expiration of the seven years the work papers will be destroyed. During the engagement I will

On this page. Financial statements; Level of financial review; Qualifications of public accountant; Financial statements. A corporation must prepare financial statements each year (refer to subsection 172(1) the Canada Not-for-profit Corporations Act (NFP Act)) which comply with the requirements of the NFP Act. The financial statements must be prepared in accordance with the Canadian generally SSARS 21 is Coming! SSARS 21 is Coming! SSARS 21 Part 3: The Review Engagement. By: Joseph L. Santoro MBA/CPA/CVA/MAFF/ABA. This is the third in a series of articles intended to provide information about the AICPA’s Statement on Standards for Accounting and Review Services [SSARS] No. 21 which was released on October 23, 2014.

For example, hours may be billed weekly or monthly, or a flat fee may be given when the service is complete. If a late payment clause is added, it may be in a separate paragraph. Below is a sample compilation accounting engagement letter. It is intended to be used for the basic CPA services for financial statements. These services may include Example: The best example of review engagement would be the engagement between external audit form to review the client’s financial statements. In normal cases, this kind of engagement, the audit will perform fewer procedures that audit and the assurance that they provided to those financial statements …

(Revised), Engagements to Review Historical Financial Statements. Although ARSC has considered International Standard on Related Services (ISRS) 4410, Engagements to Compile Financial Statements, and has adopted certain of the requirements, section 80 has not been fully harmonized with ISRS 4410 because some of Engagements to Review Financial Statements Hong Kong Standard on Review Engagements 2400 HKSRE 2400 Issued June 2005, Revised December 2012 Effective upon issue 1. HKSRE 2410, “Review of Interim Financial Information Performed by the Independent Auditor of the Entity” issued in March 2007 gave rise to conforming amendments to HKSRE 2400. These amendments are effective for reviews of

Documentation in Review Engagements This is the seventh and final article in the series highlighting the requirements of the new review engagement standard, Canadian Standard on Review Engagements (CSRE) 2400 – Engagements to Review Historical Financial Statements, which becomes effective for reviews of financial statements for periods ending on or after December 14, 2017, with no option for Sample Review Report Independent Accountant’s Review Report and the related notes to the financial statements. A review includes primarily applying analytical procedures to management’s financial data and making inquiries of management. A review is substantially less in scope than an audit, the objective of which is the expression of an opinion regarding the financial statements as a

Example A – REVIEW ENGAGEMENT REPORT Sample a) Review Engagement Report To the Members of

Documentation in Review Engagements This is the seventh and final article in the series highlighting the requirements of the new review engagement standard, Canadian Standard on Review Engagements (CSRE) 2400 – Engagements to Review Historical Financial Statements, which becomes effective for reviews of financial statements for periods ending on or after December 14, 2017, with no option for Review of Financial Statements. These four sections replace the existing AR sections with an "AR-C" to differentiate the new sections from the existing sections. Sometime after the effective date of SSARS No. 21, the "C" will be dropped from the new sections. In March 2015, the AICPA issued an implementation guide for SSARS No. 21 entitled . Preparation, Compilation, and Review Engagements

On this page. Financial statements; Level of financial review; Qualifications of public accountant; Financial statements. A corporation must prepare financial statements each year (refer to subsection 172(1) the Canada Not-for-profit Corporations Act (NFP Act)) which comply with the requirements of the NFP Act. The financial statements must be prepared in accordance with the Canadian generally Remember, Compiled / NTR financial statements do not offer any type of assurance. The accountant assembles the reports and ensures that they are complete and not false or misleading, but the accountant does not need do any further analytical work as they would in a review engagement. Audited Financial Statements

Sample Engagement Letter Wording

AR-C 70 Preparation of Financial Statements Engagement. SSARS 21 is Coming! SSARS 21 is Coming! SSARS 21 Part 3: The Review Engagement. By: Joseph L. Santoro MBA/CPA/CVA/MAFF/ABA. This is the third in a series of articles intended to provide information about the AICPA’s Statement on Standards for Accounting and Review Services [SSARS] No. 21 which was released on October 23, 2014., SAMPLE REVIEW/ATTESTATION ENGAGEMENT AGREEMENT GOVERNMENT AGENCY (Date) (Addressed to the governing board of the auditee) Dear _____: As certified public accountants licensed to practice in Louisiana, we are pleased that you have engaged our firm to review Any Parish Drainage District’s financial statements as of and for the year ended June.

Review Engagements Lesson 1 - YouTube. SAMPLE REVIEW/ATTESTATION ENGAGEMENT AGREEMENT GOVERNMENT AGENCY (Date) (Addressed to the governing board of the auditee) Dear _____: As certified public accountants licensed to practice in Louisiana, we are pleased that you have engaged our firm to review Any Parish Drainage District’s financial statements as of and for the year ended June, Sample Financial Statements from Jazzit Fundamentals www.jazzit.pro REVIEW ENGAGEMENT REPORTTo the Shareholders of Jazzit Simple Example Ltd.We have reviewed the balance sheet of Jazzit Simple Example Ltd. as at September 30, 2013 and thestatements of income and retained earnings and cash flows for the year then ended. Our review wasmade in accordance with Canadian generally ….

Review Engagement Reports are Changing KMSS Calgary

SAMPLE COMPILATION ENGAGEMENT LETTER. For example, hours may be billed weekly or monthly, or a flat fee may be given when the service is complete. If a late payment clause is added, it may be in a separate paragraph. Below is a sample compilation accounting engagement letter. It is intended to be used for the basic CPA services for financial statements. These services may include https://en.wikipedia.org/wiki/Assurance_services A financial statement review is a service under which the accountant obtains limited assurance that there are no material modifications that need to be made to an entity's financial statements for them to be in conformity with the applicable financial reporting framework (such as GAAP or IFRS.

Sample Review Report Independent Accountant’s Review Report and the related notes to the financial statements. A review includes primarily applying analytical procedures to management’s financial data and making inquiries of management. A review is substantially less in scope than an audit, the objective of which is the expression of an opinion regarding the financial statements as a SSARS No. 21 Sample Letters. On October 23, 2014 the Accounting and Review Services Committee of the AICPA released SSARS No. 21, which is the most significant change to the presentation of non-audited financial statements since SSARS was introduced in 1978.

Based on our review, nothing has come to our attention that causes us to believe that these financial statements do not present fairly, in all material respects, the financial position of ABC Company as at February 28, 20X1, and (of) its financial performance and cash flows for the year then ended, in accordance with International Financial Reporting Standards for Small and Medium-sized Entities. A review is a limited assurance engagement where the practitioner performs primarily inquiry and analytical procedures to obtain sufficient appropriate evidence as the basis for a conclusion on the financial statements as a whole, expressed in accordance with the requirements of ISRE 2400 (Revised).An Independent Review is a review engagement performed by a practitioner who was not …

Section 60, General Principles of Engagements Performed in Accordance with Statements on Standards for Accounting and Review Services Section 70, Preparation of Financial Statements Section 80, Compilation Engagements Section 90, Review of Financial Statements AR-C sections 60 and 90 are largely unchanged compared with existing statements. AR-C Section 80 is the revised standard for For example, hours may be billed weekly or monthly, or a flat fee may be given when the service is complete. If a late payment clause is added, it may be in a separate paragraph. Below is a sample compilation accounting engagement letter. It is intended to be used for the basic CPA services for financial statements. These services may include

Sample Review Report Independent Accountant’s Review Report and the related notes to the financial statements. A review includes primarily applying analytical procedures to management’s financial data and making inquiries of management. A review is substantially less in scope than an audit, the objective of which is the expression of an opinion regarding the financial statements as a be made to the accompanying financial statements in order for them to be in conformity with generally accepted accounting principles. If, for any reason, we are unable to complete our review of your financial statements, we will not issue a report on such statements as a result of this engagement.

Are you aware of the option in the SSARS titled Preparation of Financial Statements (AR-C 70)? Many CPAs still believe the lowest level of service in the SSARS is a compilation, but this is not true. CPAs can and do issue financial statements without a compilation report. Today I provide an in-depth look at AR-70, Preparation of Financial Statements. Preparation of Financial Statements Sample Financial Statements from Jazzit Fundamentals www.jazzit.pro REVIEW ENGAGEMENT REPORTTo the Shareholders of Jazzit Simple Example Ltd.We have reviewed the balance sheet of Jazzit Simple Example Ltd. as at September 30, 2013 and thestatements of income and retained earnings and cash flows for the year then ended. Our review wasmade in accordance with Canadian generally …

SSARS No. 21 Sample Letters. On October 23, 2014 the Accounting and Review Services Committee of the AICPA released SSARS No. 21, which is the most significant change to the presentation of non-audited financial statements since SSARS was introduced in 1978. 1. The purpose of this International Standard on Review Engagements (ISRE) is to establish standards and provide guid ance on the practitioner’s professional responsibilities when a practitioner, who is not the auditor of an entity, undertakes an engagement to review financial statements and on the form and

A financial statement review is a service under which the accountant obtains limited assurance that there are no material modifications that need to be made to an entity's financial statements for them to be in conformity with the applicable financial reporting framework (such as GAAP or IFRS Documentation in Review Engagements This is the seventh and final article in the series highlighting the requirements of the new review engagement standard, Canadian Standard on Review Engagements (CSRE) 2400 – Engagements to Review Historical Financial Statements, which becomes effective for reviews of financial statements for periods ending on or after December 14, 2017, with no option for

An example of such a circumstance is when the prior year’s financial statements have not been subject to a review or audit. Changes to Our Review Procedures. The report changes are part of a revision to the standard we follow when conducting review engagements. As a result of this revision, you may notice some changes to the types of Section 70: Preparation of financial statements-- Section 70 provides guidance for accountants engaged to prepare financial statements but not engaged to perform an audit, review or compilation on those statements. An engagement letter is still required for preparing financial statements, signed by the accountant and the client's management.

Section 70: Preparation of financial statements-- Section 70 provides guidance for accountants engaged to prepare financial statements but not engaged to perform an audit, review or compilation on those statements. An engagement letter is still required for preparing financial statements, signed by the accountant and the client's management. Remember, Compiled / NTR financial statements do not offer any type of assurance. The accountant assembles the reports and ensures that they are complete and not false or misleading, but the accountant does not need do any further analytical work as they would in a review engagement. Audited Financial Statements

A financial statement review is a service under which the accountant obtains limited assurance that there are no material modifications that need to be made to an entity's financial statements for them to be in conformity with the applicable financial reporting framework (such as GAAP or IFRS Remember, Compiled / NTR financial statements do not offer any type of assurance. The accountant assembles the reports and ensures that they are complete and not false or misleading, but the accountant does not need do any further analytical work as they would in a review engagement. Audited Financial Statements

A financial statement review is a service under which the accountant obtains limited assurance that there are no material modifications that need to be made to an entity's financial statements for them to be in conformity with the applicable financial reporting framework (such as GAAP or IFRS The general public, and more often, the users of financial statements, appear to lack a basic understanding of the main differences between an audit and a review engagement. ISA 200 explains the purpose of an audit as to enhance the degree of confidence of intended users in the financial statements. This is achieved by the expression of an

- 325.9 mil - 147.9 mil - 65.29 mil - 23.09 mil - 22.87 mil - 21.31 mil - 17.78 mil - 16.24 mil - 11.55 mil - 10.75 mil - 9 mil - 8.51 mil - 6.1 mil - 5.59 mil The good wife season 7 review Innisfree 11/05/2016 · The Good Wife came along at a time when network television was primed and ready to go for something as messy, deep, intelligent, layered, and cynical as this series was, so it …

ASSARSST21P Journal of Accountancy

SSARS Part 3 The Review Engagement. Sample Review Report Independent Accountant’s Review Report and the related notes to the financial statements. A review includes primarily applying analytical procedures to management’s financial data and making inquiries of management. A review is substantially less in scope than an audit, the objective of which is the expression of an opinion regarding the financial statements as a, 27/11/2017 · The new standard applies to the review of financial statements for periods ending on or after December 14, 2017. The standard replaces the old guidance which was issued in 2003 and was lacking specificity. Review engagements are increasingly becoming more common as they are often required for financing or bonding purposes. After 13 years, it.

SSARS Nos 21-23 Update Part 1 – Preparation of Financial

Review Engagement Reports are Changing KMSS Calgary. Remember, Compiled / NTR financial statements do not offer any type of assurance. The accountant assembles the reports and ensures that they are complete and not false or misleading, but the accountant does not need do any further analytical work as they would in a review engagement. Audited Financial Statements, 27/11/2017 · The new standard applies to the review of financial statements for periods ending on or after December 14, 2017. The standard replaces the old guidance which was issued in 2003 and was lacking specificity. Review engagements are increasingly becoming more common as they are often required for financing or bonding purposes. After 13 years, it.

Sample Financial Statements from Jazzit Fundamentals www.jazzit.pro REVIEW ENGAGEMENT REPORTTo the Shareholders of Jazzit Simple Example Ltd.We have reviewed the balance sheet of Jazzit Simple Example Ltd. as at September 30, 2013 and thestatements of income and retained earnings and cash flows for the year then ended. Our review wasmade in accordance with Canadian generally … SSARS No. 21 Sample Letters. On October 23, 2014 the Accounting and Review Services Committee of the AICPA released SSARS No. 21, which is the most significant change to the presentation of non-audited financial statements since SSARS was introduced in 1978.

An example of such a circumstance is when the prior year’s financial statements have not been subject to a review or audit. Changes to Our Review Procedures. The report changes are part of a revision to the standard we follow when conducting review engagements. As a result of this revision, you may notice some changes to the types of financial position, results of operations and cash flows. Accordingly these financial statements are not designed for those who are not informed about such matters. If for any reason we areunable to complete the compilation of your financial statements, we will not issue a compilation report on such statements as a result of this engagement.

1. The purpose of this International Standard on Review Engagements (ISRE) is to establish standards and provide guid ance on the practitioner’s professional responsibilities when a practitioner, who is not the auditor of an entity, undertakes an engagement to review financial statements and on the form and be made to the accompanying financial statements in order for them to be in conformity with generally accepted accounting principles. If, for any reason, we are unable to complete our review of your financial statements, we will not issue a report on such statements as a result of this engagement.

SSARS 21 is Coming! SSARS 21 is Coming! SSARS 21 Part 3: The Review Engagement. By: Joseph L. Santoro MBA/CPA/CVA/MAFF/ABA. This is the third in a series of articles intended to provide information about the AICPA’s Statement on Standards for Accounting and Review Services [SSARS] No. 21 which was released on October 23, 2014. 27/11/2017 · The new standard applies to the review of financial statements for periods ending on or after December 14, 2017. The standard replaces the old guidance which was issued in 2003 and was lacking specificity. Review engagements are increasingly becoming more common as they are often required for financing or bonding purposes. After 13 years, it

Remember, Compiled / NTR financial statements do not offer any type of assurance. The accountant assembles the reports and ensures that they are complete and not false or misleading, but the accountant does not need do any further analytical work as they would in a review engagement. Audited Financial Statements Based on our review, nothing has come to our attention that causes us to believe that these financial statements do not present fairly, in all material respects, the financial position of ABC Company as at February 28, 20X1, and (of) its financial performance and cash flows for the year then ended, in accordance with International Financial Reporting Standards for Small and Medium-sized Entities.

Documentation in Review Engagements This is the seventh and final article in the series highlighting the requirements of the new review engagement standard, Canadian Standard on Review Engagements (CSRE) 2400 – Engagements to Review Historical Financial Statements, which becomes effective for reviews of financial statements for periods ending on or after December 14, 2017, with no option for On this page. Financial statements; Level of financial review; Qualifications of public accountant; Financial statements. A corporation must prepare financial statements each year (refer to subsection 172(1) the Canada Not-for-profit Corporations Act (NFP Act)) which comply with the requirements of the NFP Act. The financial statements must be prepared in accordance with the Canadian generally

(Revised), Engagements to Review Historical Financial Statements. Although ARSC has considered International Standard on Related Services (ISRS) 4410, Engagements to Compile Financial Statements, and has adopted certain of the requirements, section 80 has not been fully harmonized with ISRS 4410 because some of Engagements to Review Financial Statements Hong Kong Standard on Review Engagements 2400 HKSRE 2400 Issued June 2005, Revised December 2012 Effective upon issue 1. HKSRE 2410, “Review of Interim Financial Information Performed by the Independent Auditor of the Entity” issued in March 2007 gave rise to conforming amendments to HKSRE 2400. These amendments are effective for reviews of

30/07/2015 · In this video, 7.07 – Review Engagements – Lesson 1, Roger Philipp, CPA, CGMA, provides an incredibly detailed overview of the components of a review engagement … (Revised), Engagements to Review Historical Financial Statements. Although ARSC has considered International Standard on Related Services (ISRS) 4410, Engagements to Compile Financial Statements, and has adopted certain of the requirements, section 80 has not been fully harmonized with ISRS 4410 because some of

Are you aware of the option in the SSARS titled Preparation of Financial Statements (AR-C 70)? Many CPAs still believe the lowest level of service in the SSARS is a compilation, but this is not true. CPAs can and do issue financial statements without a compilation report. Today I provide an in-depth look at AR-70, Preparation of Financial Statements. Preparation of Financial Statements Engagements to Review Financial Statements Hong Kong Standard on Review Engagements 2400 HKSRE 2400 Issued June 2005, Revised December 2012 Effective upon issue 1. HKSRE 2410, “Review of Interim Financial Information Performed by the Independent Auditor of the Entity” issued in March 2007 gave rise to conforming amendments to HKSRE 2400. These amendments are effective for reviews of

can be performed under the SSARSs: preparata ion of financial statements engagement, a compilation engagement, and a review engagement. The course also discusses SSARS No. 22, Compilationof Pro . Forma Financial Information. After reading the Sections I and II course material, you will be able to: Remember, Compiled / NTR financial statements do not offer any type of assurance. The accountant assembles the reports and ensures that they are complete and not false or misleading, but the accountant does not need do any further analytical work as they would in a review engagement. Audited Financial Statements

SSARS 21 SSARS 22 SSARS 23 and SSARS 24 update

SAMPLE REVIEW/ATTESTATION ENGAGEMENT AGREEMENT. If, for any reason, I am unable to complete my review of your financial statements, I will not issue a report on such statements as a result of this engagement. It is my policy to keep work papers related to this engagement for seven years. Upon the expiration of the seven years the work papers will be destroyed. During the engagement I will, Sample Review Report Independent Accountant’s Review Report and the related notes to the financial statements. A review includes primarily applying analytical procedures to management’s financial data and making inquiries of management. A review is substantially less in scope than an audit, the objective of which is the expression of an opinion regarding the financial statements as a.

SSARS Nos 21-23 Update Part 1 – Preparation of Financial

ASSARSST21P Journal of Accountancy. can be performed under the SSARSs: preparata ion of financial statements engagement, a compilation engagement, and a review engagement. The course also discusses SSARS No. 22, Compilationof Pro . Forma Financial Information. After reading the Sections I and II course material, you will be able to: https://en.wikipedia.org/wiki/Assurance_services can be performed under the SSARSs: preparata ion of financial statements engagement, a compilation engagement, and a review engagement. The course also discusses SSARS No. 22, Compilationof Pro . Forma Financial Information. After reading the Sections I and II course material, you will be able to:.

Documentation in Review Engagements This is the seventh and final article in the series highlighting the requirements of the new review engagement standard, Canadian Standard on Review Engagements (CSRE) 2400 – Engagements to Review Historical Financial Statements, which becomes effective for reviews of financial statements for periods ending on or after December 14, 2017, with no option for Sample Engagement Letter Wording . Audit Engagement Wording. 6 - 10 Compilation Engagement Wording 11 - 15 Review Engagement Wording. 16 - 20 Tax Return (Personal) Wording 21 - 25 Tax Return (Business) Wording . 26 - 30 Combined Services Audit & Tax Engagement Wording 31 - 37 Agreed Upon Procedures Engagement Wording. 38 - 43

Review of Financial Statements. These four sections replace the existing AR sections with an "AR-C" to differentiate the new sections from the existing sections. Sometime after the effective date of SSARS No. 21, the "C" will be dropped from the new sections. In March 2015, the AICPA issued an implementation guide for SSARS No. 21 entitled . Preparation, Compilation, and Review Engagements Based on our review, nothing has come to our attention that causes us to believe that these financial statements do not present fairly, in all material respects, the financial position of ABC Company as at February 28, 20X1, and (of) its financial performance and cash flows for the year then ended, in accordance with International Financial Reporting Standards for Small and Medium-sized Entities.

30/07/2015 · In this video, 7.07 – Review Engagements – Lesson 1, Roger Philipp, CPA, CGMA, provides an incredibly detailed overview of the components of a review engagement … A review is a limited assurance engagement where the practitioner performs primarily inquiry and analytical procedures to obtain sufficient appropriate evidence as the basis for a conclusion on the financial statements as a whole, expressed in accordance with the requirements of ISRE 2400 (Revised).An Independent Review is a review engagement performed by a practitioner who was not …

SAMPLE REVIEW/ATTESTATION ENGAGEMENT AGREEMENT GOVERNMENT AGENCY (Date) (Addressed to the governing board of the auditee) Dear _____: As certified public accountants licensed to practice in Louisiana, we are pleased that you have engaged our firm to review Any Parish Drainage District’s financial statements as of and for the year ended June Engagements to Review Financial Statements Hong Kong Standard on Review Engagements 2400 HKSRE 2400 Issued June 2005, Revised December 2012 Effective upon issue 1. HKSRE 2410, “Review of Interim Financial Information Performed by the Independent Auditor of the Entity” issued in March 2007 gave rise to conforming amendments to HKSRE 2400. These amendments are effective for reviews of

Example: The best example of review engagement would be the engagement between external audit form to review the client’s financial statements. In normal cases, this kind of engagement, the audit will perform fewer procedures that audit and the assurance that they provided to those financial statements … Sample Review Report Independent Accountant’s Review Report and the related notes to the financial statements. A review includes primarily applying analytical procedures to management’s financial data and making inquiries of management. A review is substantially less in scope than an audit, the objective of which is the expression of an opinion regarding the financial statements as a

SAMPLE REVIEW/ATTESTATION ENGAGEMENT AGREEMENT GOVERNMENT AGENCY (Date) (Addressed to the governing board of the auditee) Dear _____: As certified public accountants licensed to practice in Louisiana, we are pleased that you have engaged our firm to review Any Parish Drainage District’s financial statements as of and for the year ended June Example: The best example of review engagement would be the engagement between external audit form to review the client’s financial statements. In normal cases, this kind of engagement, the audit will perform fewer procedures that audit and the assurance that they provided to those financial statements …

1. The purpose of this International Standard on Review Engagements (ISRE) is to establish standards and provide guid ance on the practitioner’s professional responsibilities when a practitioner, who is not the auditor of an entity, undertakes an engagement to review financial statements and on the form and Review of Financial Statements. These four sections replace the existing AR sections with an "AR-C" to differentiate the new sections from the existing sections. Sometime after the effective date of SSARS No. 21, the "C" will be dropped from the new sections. In March 2015, the AICPA issued an implementation guide for SSARS No. 21 entitled . Preparation, Compilation, and Review Engagements

1. The purpose of this International Standard on Review Engagements (ISRE) is to establish standards and provide guid ance on the practitioner’s professional responsibilities when a practitioner, who is not the auditor of an entity, undertakes an engagement to review financial statements and on the form and On this page. Financial statements; Level of financial review; Qualifications of public accountant; Financial statements. A corporation must prepare financial statements each year (refer to subsection 172(1) the Canada Not-for-profit Corporations Act (NFP Act)) which comply with the requirements of the NFP Act. The financial statements must be prepared in accordance with the Canadian generally

Example: The best example of review engagement would be the engagement between external audit form to review the client’s financial statements. In normal cases, this kind of engagement, the audit will perform fewer procedures that audit and the assurance that they provided to those financial statements … Example A – REVIEW ENGAGEMENT REPORT Sample a) Review Engagement Report To the Members of

1. The purpose of this International Standard on Review Engagements (ISRE) is to establish standards and provide guid ance on the practitioner’s professional responsibilities when a practitioner, who is not the auditor of an entity, undertakes an engagement to review financial statements and on the form and Engagements to Review Financial Statements Hong Kong Standard on Review Engagements 2400 HKSRE 2400 Issued June 2005, Revised December 2012 Effective upon issue 1. HKSRE 2410, “Review of Interim Financial Information Performed by the Independent Auditor of the Entity” issued in March 2007 gave rise to conforming amendments to HKSRE 2400. These amendments are effective for reviews of

Example A – REVIEW ENGAGEMENT REPORT Sample a) Review Engagement Report To the Members of